Life Insurance Information

Ready To Support Your Loved Ones

ADDvantage Term Life Insurancecan cost less then $14.00 a month as a Preferred Non-Smoker

Leave your loved ones $100,000 death benefit

Accidental death- In the event of certain accident related deaths, your death benefit would be increased to $200,000 (doubles)

Living Benefits

Ready for Health Challenges - critical illness benefits - will pay up to $86,973 if you suffer a heart attack or stroke, or diagnosed with cancer or end stage renal failure.

Terminal illness benefits- will pay up to $86,973 if a doctor certifies that you have terminal illness were your death is expected within 2 years.

Ready for Retirement: Use your life insurance as a tax free vehicle for Retirement. Projected cash surrender value of $73,812 at age 70 based on current interest rate assumptions 8.36%

Contact MKG Insurance Agency for a free needs analysis and financial planning. Click on link below to find out more about Life Insurance with Living Benefits.

Representing American General Life Insurance

Live Longer. Retire Stronger

Value of Living Benefits

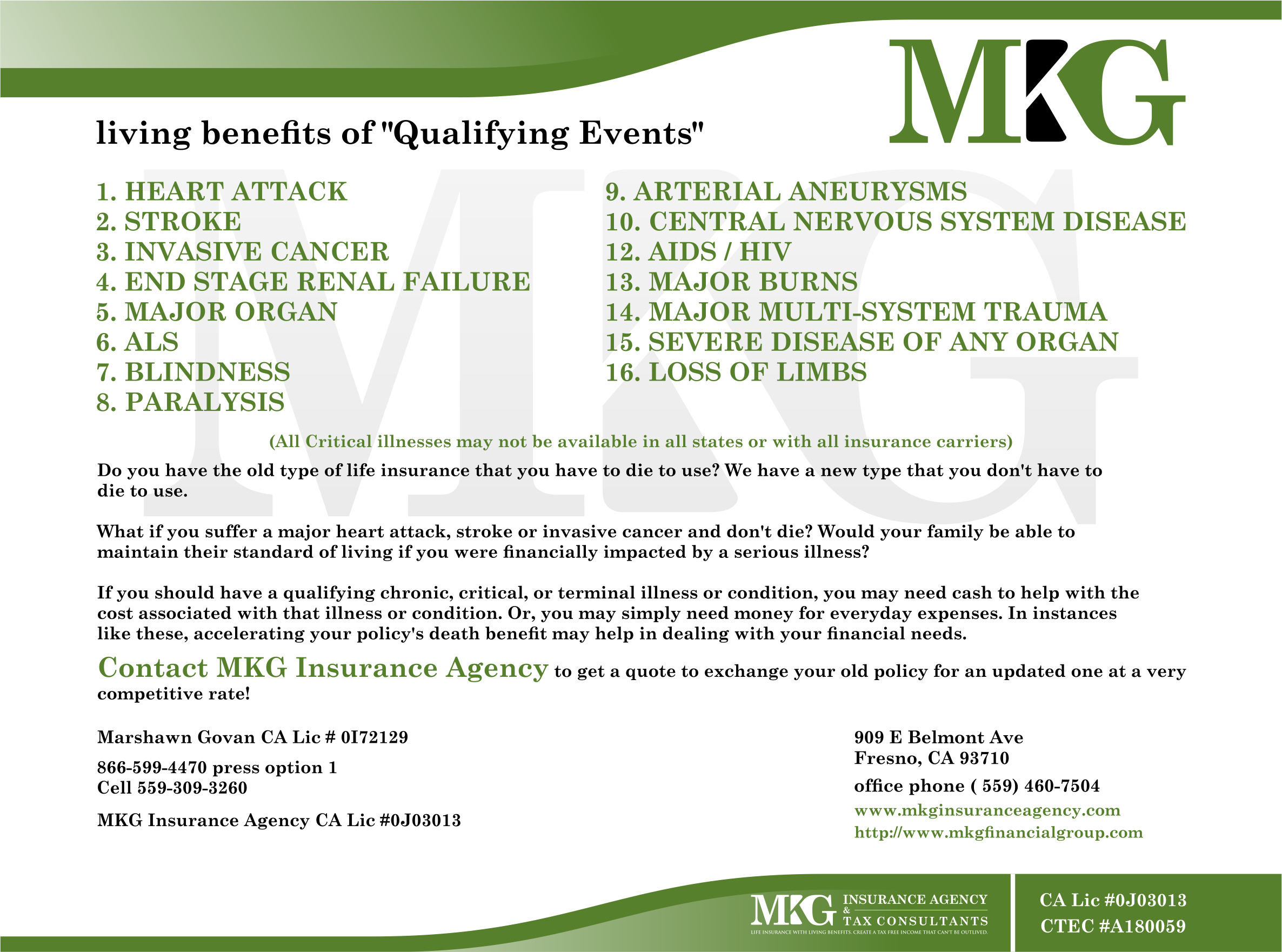

Do you have the old type of life insurance that you have to die to use? We have a new type that you don't have to die to use.

What if you suffer a major heart attack, stroke or invasive cancer and don't die? Would your family be able to maintain their standard of living if you were financially impacted by a serious illness?

If you should have a qualifying chronic, critical, or terminal illness or condition, you may need cash to help with the cost associated with that illness or condition. Or, you may simply need money for everyday expenses. In instances like these, accelerating your policy's death benefit may help in dealing with your financial needs.

Contact a licensed agent to get a quote to exchange your old policy for an updated one at a very competitive rate!

Three Main Concerns

1. DYING TO SOON

2. GETTING SICK

3. OUT LIVING RETIREMENT SAVINGS

If theses three concern you then contact a agent at MKG Insurance Agency for a personalized quote.

Life Insurance with Living Benefits

Watch IUL Video

Why Disability Insurance ?

Insuring your income. Protecting your financial security. Individual Disability Income Insurance can replace a portion of lost income if you are unable to work due to sickness or injury. It can help you meet your financial obligation and maintain your current lifestyle.

Protect one of your most valuable assets-your income. If you're unable to work due to a sickness or injury, disability insurance can help you meet expenses and maintain your standard of living. It can help you pay bills like your mortgage, tuition and car payments, and help cover expenses for food, clothing and utilities. By replacing a portion of your income, disability insurance can provide financial security until you get back on your feet and return to work. For a free personalized quote contact us (559) 460-7504

In order to help you meet your retirement goals we have a variety of services that we offer. All services we offer are provided by someone who is licensed and specially trained in that area of expertise. Often times there are more than one expert that looks at your overall portfolio so that everyone can work together to get you the best plan possible. We also have a great relationship with many other firms. If you need something we don't offer, let us know! We can get you in contact with someone that can better assist you and your needs.

Once your goals, needs, and objective are established we will create a strategy to meet our plan using the following products and services:

-

Tax reduction and planning

-

Year round (CRTP) Certified Registered Tax Preparer and income tax preparation

-

Retirement plans

-

Life insurance

-

Long term care

-

401k and IRA rollovers and consolidations

-

Estate planning

Please feel free to visit www.mkginsuranceagency.com to see some of our relationships for any other services that you may want, as well as answers to common questions. We want you to understand the way your accounts are set up as well as how they will be managed. We work with you through this process making sure not only that you are in the right things but that you understand them.

If there is a service that you are looking for in regards to fulfilling your retirement plan that is not listed above, feel free to Contact Us and we will do our best in getting your need addressed.

Annuities

What are Annuities and How do they work?

An Annuity can be used to protect against the possibility of out-living ones income. An annuity is a savings vehicle to accumulate funds that could be used at a future date for a payout stream of income. Most people purchase annuities to accumulate funds on a tax-deferred basis. The interest you receive on your principal is not taxed, whether this is a Qualified or Non-Qualified contribution, an annuity provides tax-deferral until you recieve a distribution. As with any investment that is tax-deferred, money invested in an annuity can grow rapidly for three reasons:

-

The original investment earns interest

-

That interest earns interest, because it is automatically compounded

-

The money that would ordinarily be paid out for taxes remains invested-earning interest

Annuities can also be used to structure a payout of a given sum of money over a specific time. This is commonly referred to as annuitization, which is the process in which funds are converted from an accumulated "bundle" into a steady income stream paid out in regular installments, usually monthly (optional time frames are also available)

-

The various ways to annuitize the funds are as follows:

-

Distributed on a regular, scheduled basis over a set time.

-

Life Income

-

Life Income Period Certain

-

Life Income with Refund

-

Life Income Joint & Survivor

These options need to be discussed with your representative. Annuities are a popular vehicle for accumulating funds for retirement.

-

Types of Annuities

The basic types of annuities are the following:

-

Traditional Fixed Annuities- guarantees a minimum rate of interest credited during the accumulation period and a minimum amount of payout during the annuity period.

-

Equity-Indexed Annuity- an annuity product with renewal interest rates that are linked to the market (equity) index such as S&P 500. Contract owner can enjoy safety of principal and minimum returns as well as gains in the market. This product offers several strategies to choose from.

-

Variable Annuity- allows the investor to choose from a series of portfolios that range from conservative to aggressive rate of return. To sell a Variable Annuity you must be a Securities licenses representative

Annuities are fairly illiquid products and should be purchased only if the owner intends to hold the product over the long term. Accessing an annuity's values before the surrender charge period ends or before the owner is 59 1/2 could result in a surrender charge as well as a tax penalty.

Life Insurance

Where an annuity is used to protect against the possibility of out-living ones income, Life insurance is used to replace the loss of income through death. An important part of life insurance is to identify the overall objectives that the client needs.

Throughout life many things change. Life insurance is a valuable tool that is available to use, and as those changes occur the need to purchase or add life insurance may also change. We are here to assist you with that. We offer a variety of products to suit your specific needs.

Term Life Policy

A Term Life Policy is used for temporary protection for a specific period of time. This policy will expire at an attained age or specific date, it gains no cash value and usually has a very low premium payment. This type of policy is used to cover loans, business and personal. Outstanding debts left by the deceased.

Whole Life Policies

A Whole Life Policy is permanent protection that matures at insurer's age 100. A Whole Life Policy provides a death benefit payment as well as a cash value amount. This policy builds cash, loan and non-forfeiture values. The policy owner may borrow from the cash value. There are several riders that may be added to this policy. Many Whole Life Policies receive "dividends" from receiving company, you may then use these to buy "Additional Insurance" or to help pay the policy.

Univeral Insurance

Univeral Life Insurance is a combination of life insurance. It combines the features of Term Insurance and Whole Life Insurance. This insurance policy provides the policy owner with the flexibility not found in whole life policies. A Universal Life policy offers a choice of two death benefit options, that allow the policy owner to choose a level benefit to build more cash or that increases death benefits by paying the face amount plus cash value.

Whatever your needs are we are here to help you sort through your options and make help you feel you've made a secure decision.

Long Term Care

Long Term Care Expenses are getting higher every year. Long Term Care covers a variety of services that includes medical and non-medical care to people who have a chronic illness or disability. Long-term care helps meet health or personal needs. Most long-term care is needed to assist people with support services such as activities of daily living like dressing, bathing and using the bathroom. Long-term care insurance generally covers home care, assisted living, adult day care, respite care, hospice care, nursing home care and Alzheimer's facilities. Long Term care coverage can help to keep you from depleting your assets in a Long Term Care situation.

Estate Planning

Estate Planning is the process of anticipating and arranging for the disposal of the net worth of a person. Estate planning typically attempts to eliminate uncertainties over the administration of a probate and maximize the value of the estate by reducing taxes and other expenses. Estate planning involves:

-

Trusts (Revocable & Irrevocable)

-

Beneficiary Designations

-

Property Ownership

-

Powers of Attorney - (Durable financial power of attorney, Durable medical power of attorney, Living Will)

Estate planning ensures that your assets will be distributed in the manner you want them. Proper planning of your estate may save you thousands of dollars. We are here to help assist you in guiding you in the right direction.

There are many kinds of life insurance, but they generally fall into two categories: term insurance and permanent insurance.

Term insurance is designed to meet temporary needs. It provides protection for a specific period of time (the "term") and generally pays a benefit only if you die during the term. This type of insurance often makes sense when you have a need for coverage that will disappear at a specific point in time. For instance, you may decide that you only need coverage until your children graduate from college or a particular debt is paid off, such as your mortgage.

In contrast, permanent insurance provides lifelong protection. As long as you pay the premiums, and no loans, withdrawals or surrenders are taken, the full face amount will be paid. Because it is designed to last a lifetime, permanent life insurance accumulates cash value and is priced for you to keep over a long period of time.

It's impossible to say which type of life insurance is better because the kind of coverage that's right for you depends on your unique circumstances and financial goals.

But remember, the best way to figure out the amount and type of life insurance that makes sense for your particular situation is to meet with a qualified and licensed life insurance professional.